Wild Bear Market Swings Continue With The Biggest 2 Day Rally Since April 2020

Wild Bear Market Swings Continue With The Biggest 2 Day Rally Since April 2020

A September Recap. It's a Tough Environment to Trade

In the last three weeks of September, the S&P 500 fell 13.3%, and closed out the day, week, month, and quarter at 52 week lows. It was the first 3-quarter loss since the great financial crisis of 2008, the worst month since the Covid crash, and the worst September since 2002.

There was plenty of bad news for equity investors behind this: on the 13th, CPI came in hotter than expected again, only slightly, even as gasoline prices fell substantially. This wrecked the growing hopes for a Fed pivot. They delivered a third 75bp rate hike 8 days later, with a much gloomier Summary of Economic Projections (quarterly report) and some blunt comments from Jerome Powell about needing a difficult housing correction.

The UK then delivered another blow, on the 23rd, spooking markets with the new Liz Truss government announcing the her economic plan which would have required a massive increase in borrowing. The Pound sterling plunged to record lows against the Dollar, and the S&P tapped the June bottom the same day.

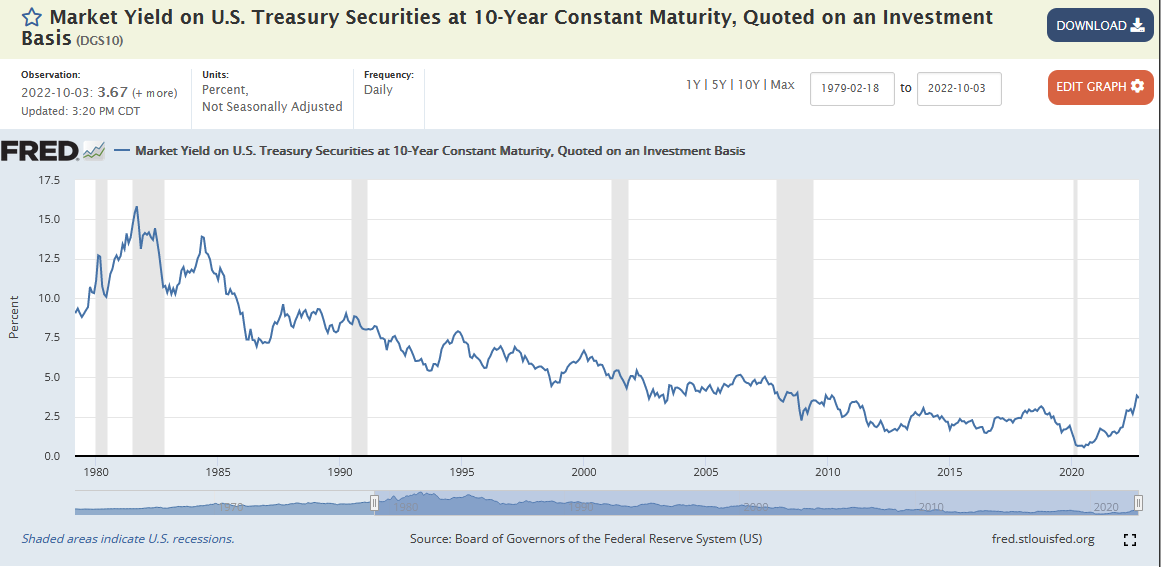

The whole month, yields on U.S. government bonds continued to rise sharply above the 40 year downtrend:

On the 26th, we got more uncertainty coming out of Europe with explosions disabling Nordstream 1 & 2, underwater gas pipelines. It appears to be sabotage but it’s an escalation by an as of yet unknown, probably state actor.

With the pound still slipping, the Bank of England intervened with an announcement to buy bonds on the 28th, the first major sign of possible central bank capitulation. English pensions, overloaded with leverage, faced potential margin calls and that’s not a meltdown they were ready to tolerate. The dollar -over extended and at 20 year highs- finally began to pull back. Stocks surged, but only for a day.

Apple - the largest stock by market cap and widely considered one of the safest stocks - spent the second half of the month with bulls defending a range near the $150/20 day moving average level while the rest of the market fell. Late on September 27th, they announced they too were experiencing falling demand, and cut iPhone 14 production plans. It cratered to about $138, a 7.7% drop in the final week. I watched it slice through the $140 and $145 lines in real time with zero hesitation, and it even closed Friday underneath the Covid-June lows trend-line. At key psychological levels, you simply could not find any buyers waiting. The S&P 500 index (SPX) and SPY closed slightly underneath the 200 week moving average also, although futures did not.

Tesla, the other mega-cap bull holdout (especially for retail investors), brought weekend news at the start of October that their record deliveries were not record enough. Investors priced in a bigger beat, so we knew to expect disaster, and it delivered an 8.6% fall on Monday.

With that backdrop, I should have still been short the market, but I exited my bearish trade a bit early on the 22nd after hitting some important targets I set. As stated in that last update on the 26th, things looked oversold, and I was sort of expecting at least a little bear market rally.

Well we got that in the first trading days of October! It’s the biggest 2 day gain since the pandemic. What overcame Tesla’s drag? The U.K. scrapped part of the economic plan that spooked markets, and we have seen continued correction the the bond and dollar charts. The UN and IMF called on the Fed to stop the aggressive rate hiking, and job openings fell the most since the pandemic, fueling the “this time the Fed will pivot” mania again.

Just like that, we moved right back to the middle of the 2022 bear channel and bounced fairly cleanly off the 200 week moving average. We’re almost back to the 20-day moving average (yellow line).

I’m feeling a little stupid for not taking a bullish trade, such as buying long dated SQQQ puts, but with so much instability in bonds, currencies, and the Nordstream news, it felt like something else could break any minute, and cause a panic leg down in stocks as we have seen before. Bearish sentiment wasn’t at record highs, and we were still comfortably above the S&P’s 3400 range at the bottom of the bear channel.

We have just went through one of the longest periods of the cheapest money in history, done in unison by central banks across the globe. The leverage and malinvestment that this has created is probably unprecedented. Now, with the absurd reaction by governments to the pandemic, the inflation beast has awakened like we haven’t seen in four decades. Central banks are trying to unwind, taking extra care to telegraph their moves in attempt to keep things orderly, but they are on a collision course with the unsustainable investments they encouraged everyone to make. The ZeroHedge article I linked in the last paragraph is very much worth a read.

So is the latest post a the The Baerlocher Bearing, where Alan concludes with a note of caution regarding the Fed pivoting:

The problem is that the Fed is prepared for employment to go soft. The Fed has a singular mandate now and that mandate to is reduce inflation. This was made plainly obvious by NY Fed President John Williams yesterday in his speech in Arizona.

“To help rein in demand to levels consistent with supply—and therefore bring inflation down—monetary policy needs to do its job. The FOMC is taking strong actions toward that end.

At its most recent meeting, in September, the FOMC raised the target range of the federal funds rate to 3 to 3-1/4 percent, its fifth consecutive increase.4 And the Committee said it anticipates that ongoing increases will be appropriate.”

(…)

“As a result of slowing growth, I anticipate the unemployment rate will rise from its current level of 3.7 percent to around 4-1/2 percent by the end of 2023.”

“Tighter monetary policy has begun to cool demand and reduce inflationary pressures, but our job is not yet done. It will take time, but I am fully confident we will return to a sustained period of price stability.”

This does not sound like a man who is ready to sign off on a change of course in monetary policy because job openings have cooled off. Expect the market to continue to interpret the signs wrong and push higher.

I might add, John Williams historically has been one of the Fed’s doves.

Next week we get FOMC minutes and CPI. Perhaps that’s when the bears will regain control.

While I know this rally can't have legs, history is on the side of finishing the year strong.

https://twitter.com/charliebilello/status/1577000937990025216

Love reading your analysis of market action. It really helps me make sense of things. Thank you!!!