For Investors, Cash is Not Trash, and More

For Investors, Cash is Not Trash, and More

Patience is key

Cash is Not Trash

Markets have reacted much more rationally to moves by the Federal Reserve to tighten money supply now that we are 7 rate hikes into this process. Recall that during the summer, everyone was in shock from record high YoY CPI of 9.1% and stunned by the Fed’s aggressive June 75bps hike which was only supposed to happen once. Then July monthly inflation came in at 0% and there was a euphoric mania in stocks that sent them into obviously overbought conditions. The market rebellion against Jerome Powell’s steady signals resulted in the chairman discarding his traditionally lengthy, more academic Jackson Hole speech for a short, stern rebuke. That whole episode made for some easy trades that I was sadly just testing out and not yet ready to swing full size on.

Since then, the swings have continued but overall volatility has decreased. If you think about it, it’s kind of funny, or pathetic, how dominated traders and investors are by every bit of news being analyzed and reacted to for how it will change the dealer’s money printer’s next move. Instead of actually investing based on which companies are producing the most value, we’re more focused on chasing what liquidity the central planners grant us today - what a waste - but that’s what monetary central planning brings about. Anyway, the point is - we haven’t seen the same clear signs of an overbought stock market defying reality to the degree seen in August. It never reached similarly oversold conditions either (the October 13th lows didn’t reach the bottom of the year’s main channel). Even the market pumpers notice how orderly things have been so far, relative to the intensity of the rate hikes:

I’ve toyed with a few more one-sided 3x ETF puts and taken most of them off the table already with small profits, thankfully. The one I have held since 11/4, a $53 UDOW put expiring 6/16/23, is still slightly underwater. I just don’t have much conviction in the short term, and have to keep reminding myself cash isn’t trash when you don’t see something good to invest in. Better wait for a good opportunity than take shots in the dark.

Follow-up on Leveraged ETF Research

I was hoping, with the volatility index returning to the low 20’s, that if now was an uncertain time in the markets, at least I can bet against the dumpster fire the leveraged ETF space is while puts are relatively cheaper. After looking at it more carefully, I concluded patience will again be key here.

Here are a few additional thoughts on what signals might indicate it’s time to start buying puts. Let’s consider the VIX first. Options are cheaper when volatility is lower, and more expensive when volatility is higher. So it would be nice to have a low VIX coincide with a relatively overpriced leveraged ETF. That would be a sign to take on more risk through a larger trade or shorter expiration.

However, even more important in options trading is the price of the underlying asset. You want to catch it moving in your favor in as large and as quick of a way as possible. That’s why the RSI will be my number one signal in making these trades. VIX will be secondary.

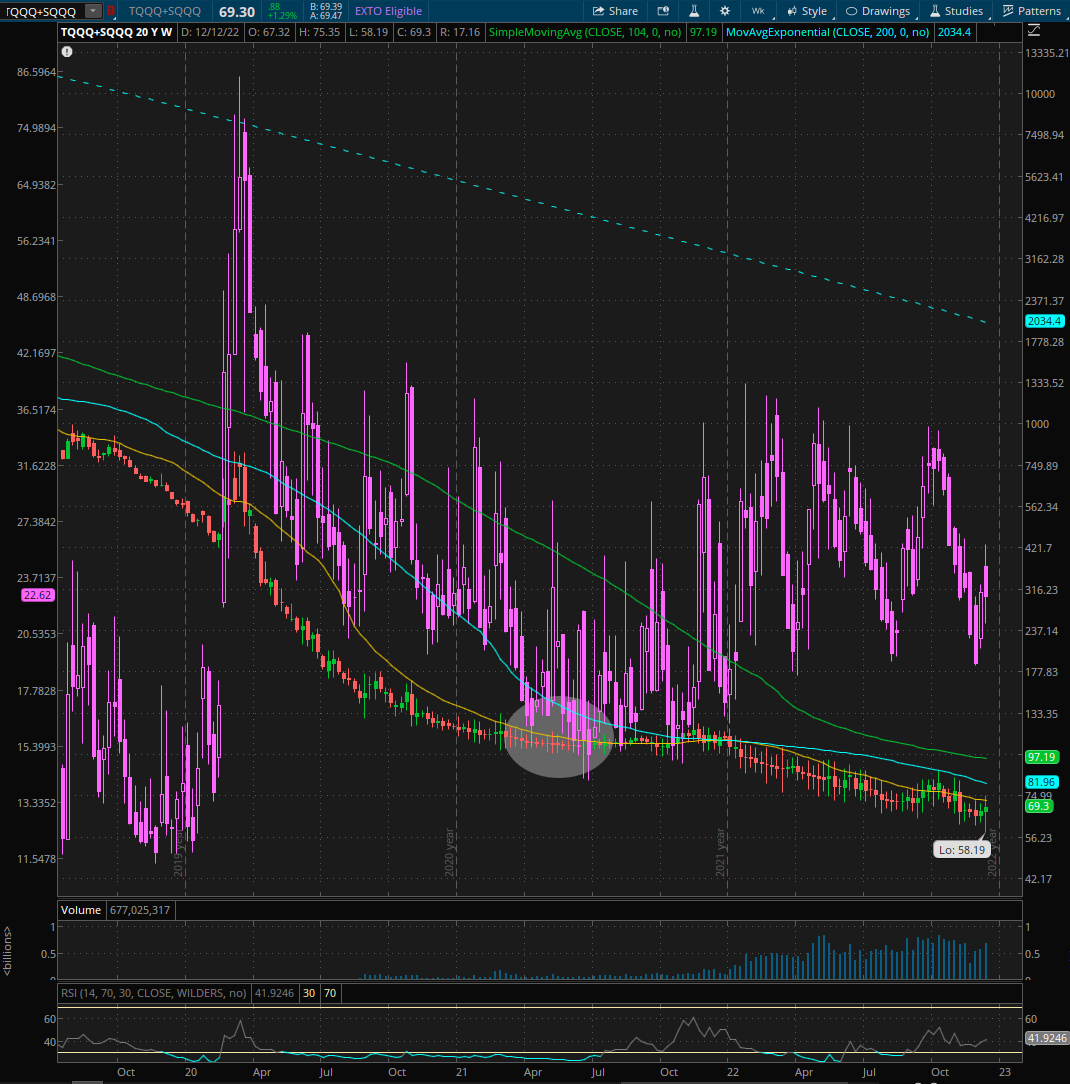

There are many examples where low VIX does not correlate with the normal rate of price decay on the ETF combos. Starting in early summer 2021, TQQQ+SQQQ price remained stable for the rest of the year even as VIX reached lows ranging from 14-20. If you bought your puts then, theta decay would have meant a losing trade for possibly 12 months. Waiting to buy until November would have been ideal, and that’s exactly when the weekly RSI hit 60, a historically high number for the combo.

(All images: Purple candles are VIX, left axis is VIX pricing; right axis is option price).

SPXL+SPXS, in the same time frame, highlights an even more dramatic case of the combo price rising for an extended time under low VIX:

A more zoomed out view would show that combo shouldn’t be touched unless weekly RSI is at least 70.

Many more examples exist, and each time, low VIX and low RSI was a bad combination. I’ll leave you with one more, from summer 2018 (highlighted), of SOXL+SOXS:

It’s not easy, at least with TD Ameritrade’s Think or Swim, to review the price history for most puts on these ETF’s because they are so thinly traded. That makes it hard to compare the VIX, but here’s one from the more thickly traded TQQQ $50 1/20/23 puts. One of the best couple of months to buy this trade included weeks where the VIX ranged from sub-20 to 35 in late November 2021. Whether you pay $4 or $6 for your put is practically immaterial when it quickly goes to $15 and later $30+.

I’m willing to work up to larger than just a few percent of my portfolio under some conditions. One approach is to set a weekly RSI target - say 65, and buy the longest dated, at the money (ATM) put available. If the price keeps increasing, set a higher RSI target (70?) and buy another ATM put (which will be a higher strike than the last one) but get a medium term expiration. Finally, if the price continues to spike further, a final layer of ATM puts with short expirations can be added. Once the price reversed, you would unload the shortest dated puts first and the longest dated puts last. This “triangle” shaped trade could have more or less layers.

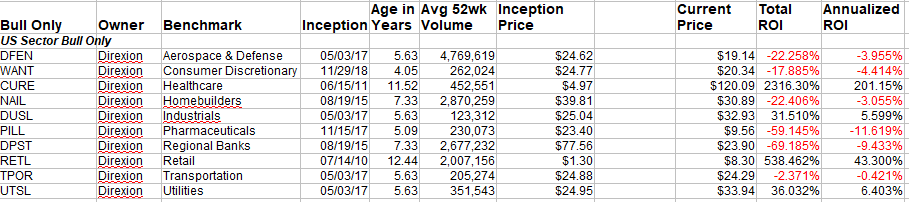

Finally, there are some 3x bull ETF’s for US sectors that don’t have a corresponding bear ETF. They went unmentioned in the last post, but I compiled data as of 12/10/22 on them as well (see below). Alerts have been set on their weekly RSI also, but at a much higher level. I would consider trading against them at extreme overbought conditions, depending on other macro economic data.

I welcome feedback as I continue to refine my thinking on all this.

An Unsuccessful Trade

I have held FCX shares since the good ‘ole days when the late Robert Wenzel of Economic Policy Journal recommended it and a slew of other stocks. My cost basis was $33. It rose as high as $51.99 just over a year later before falling with the rest of the market, briefly cracking under $25 this July. Seeing it red for a few months became intolerable and I finally decided to farm premium when it flashed over $33 again on October 26.

However, I missed an important trend. FCX is a metals mining company, primarily in copper but also gold and molybdenum. The dollar index topped out in late September, and began a reversal that continues to this day in anticipation of the Federal Reserve slowing down on rate increases. That gave metals like gold and copper breathing room to finally start moving up again. My sold call option expired this week, which would have me selling shares at breakeven but keeping all the premium at a profit.

I ended up rolling the call last minute, taking a small loss of $0.85/share. I sold a new contract for a higher strike price ($36), which will more than cover the loss. Now we have till 2/17/23 to see how this plays out - I believe with recession themes becoming stronger this might work - and if not I’ll still have more profits to pocket anyway.

*Disclaimer: This post discusses investment strategies but is not a personalized investment recommendation. Readers are responsible for their own research and risk assessment decisions when investing.*

What a great idea to use RSI along with the VIX!